Erik Norland and Oliver Andrews, CME Group

At a Glance:

- Employment reports, particularly the nonfarm payroll jobs growth number (NFP), have the most significant impact on trading volumes in interest rate futures and options.

- Despite the post-pandemic inflation surge, retail sales data has emerged as the second most influential economic indicator for traders.

Economic data sets that can have potential implications on monetary policy, reflect the state of the economy, pace of inflation and conditions in the labor market tend to impact markets in varying degrees. The timing of these data sets’ release can also be crucial in influencing investors with their portfolio decisions.

For instance, there is now a growing focus on the next step in the Federal Reserve’s path on monetary policy amid the uncertainties of trade policy, so particular attention is given to its interest-rate setting meetings. Which economic data sets get the most attention among investors in driving trading volumes in interest rate futures and options – inflation, employment or other data like retail sales?

When economic data is announced, traders, and their algorithmic tools, immediately compare the actual figures versus consensus market forecasts. The difference, often called the “surprise,” can trigger volatility as traders adjust their outlooks and rebalance positions.

Our analysis uses the multiple linear regression (MLR) statistical technique to assess how the “surprise” in U.S. data series (difference between market expectations and actual outcomes) correspond to subsequent trading volume from January 2021 to January 2025. While details on the full analysis and methodology can be found here, five key findings are summarized below.

1. Despite the 2021-2022 inflation surge, traders reacted more to employment reports than to headline or core CPI surprises over the past four years. They also traded more on surprises in retail sales – consumer spending accounts for more than two-thirds of U.S. economic activity – than on CPI.

2. Surprises in labor, inflation and retail sales data consistently showed statistically significant impacts on trading volumes in the first one, five and 10 minutes.

The 1-minute results were particularly striking. On days with no economic data releases or when data showed no surprises versus consensus, in the first minute after the report (8:30:00 - 8:30:59), on average about 20,663 interest rate futures contracts were traded. A one standard deviation surprise in NFP in either direction led to 174,173 additional contracts traded above average between 8:30:00 - 8:30:59.

In the minute after the reports’ releases, surprises in related labor market data, such as the unemployment rate and average hourly earnings, also produced strong impacts on interest rate volumes, as did initial jobless claims, ranging from 80,000 to 145,000 in additional futures volumes for a one standard deviation miss from consensus. The impact on options volumes during the first minute after the releases were typically much smaller.

3. Retail sales have been the second most influential piece of data after the employment numbers. A one standard deviation surprise versus forecasts on retail sales typically produced an additional 80,000 contracts of futures volume in the minute after release.

4. Despite the post-pandemic surge in inflation, market reactions to surprises in CPI, core CPI and PPI, although still statistically significant, tended to be more muted, adding only 20,000 to 30,000 contacts to the futures trading volume within a minute of their release. They tended to have a mixed and negligible immediate impact upon options volumes.

5. Recognizing that FOMC policy announcements can significantly influence trading activity, we included a dummy variable to account for these days. Interest rate options daily trading volume is, on average, 1,747,832 contracts higher on FOMC announcement days compared to non-FOMC days.

2021-2025: A Period of Change

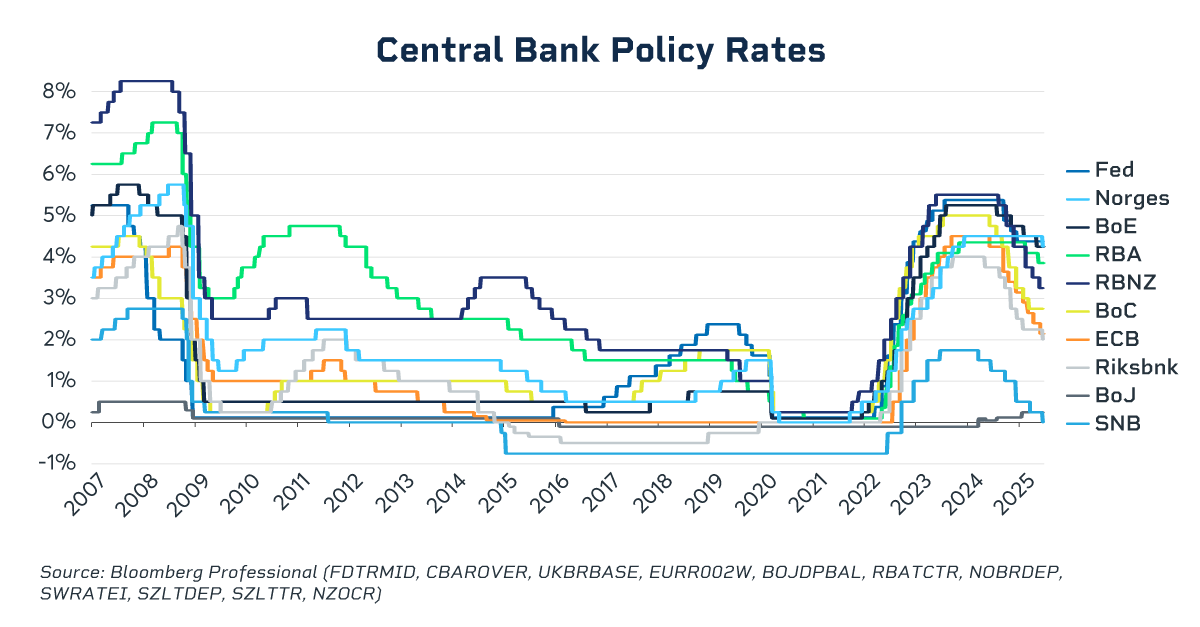

Since 2021, financial markets have experienced significant uncertainty about future interest rates, mostly because inflation rose sharply after the pandemic. Core PCE, the Fed’s preferred inflation measure, exceeded the 2% target, hitting 3.1% in May 2021 and peaked at 5.3% in March 2022. Core PCE was 2.9% in January 2025.

To control inflation, the U.S. Fed started raising interest rates from March 2022 onward and was followed by many of its peers around the world:

In analyzing these dynamics, market participants can gain a better understanding of market reactions to economic data, which may ultimately support more informed decision-making.

CME Group futures are not suitable for all investors and involve the risk of loss. Full disclaimer. Copyright © 2025 CME Group Inc.