Over the last few decades, we have seen the secondary market evolve drastically. As institutional portfolios have grown in size and complexity, limited partners (“LPs”) have increasingly sought out tools to actively manage exposures and respond to market conditions. As private equity distributions remain challenged and overallocation pressures persist, LPs are increasingly considering the liquidity tools available in their tool set. LP Financing Solutions have emerged as a flexible, structured alternative that enable LPs to generate liquidity without sacrificing strategic relationships or long-term upside potential. A creative tool in the tool set… and one that could become increasingly important for allocators actively managing their portfolios.

An Overview of LPs’ Rising Liquidity Needs

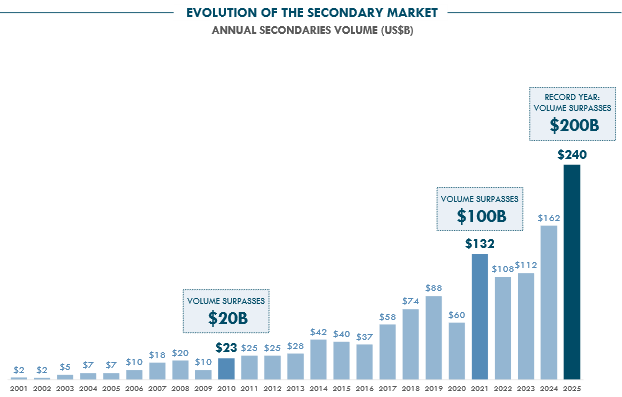

The Evolution of the Secondary Market

In public markets, a secondary market for listed equities has existed since the late 18th century, providing investors with liquidity and price discovery.

In private markets, we have seen the secondary market evolve drastically over the last few decades. From the late 1990s into the early 2000s, secondary sales of private equity interests were often viewed as a liquidity solution of last resort — often interpreted as a signal of a seller’s distress or structural liquidity challenges.

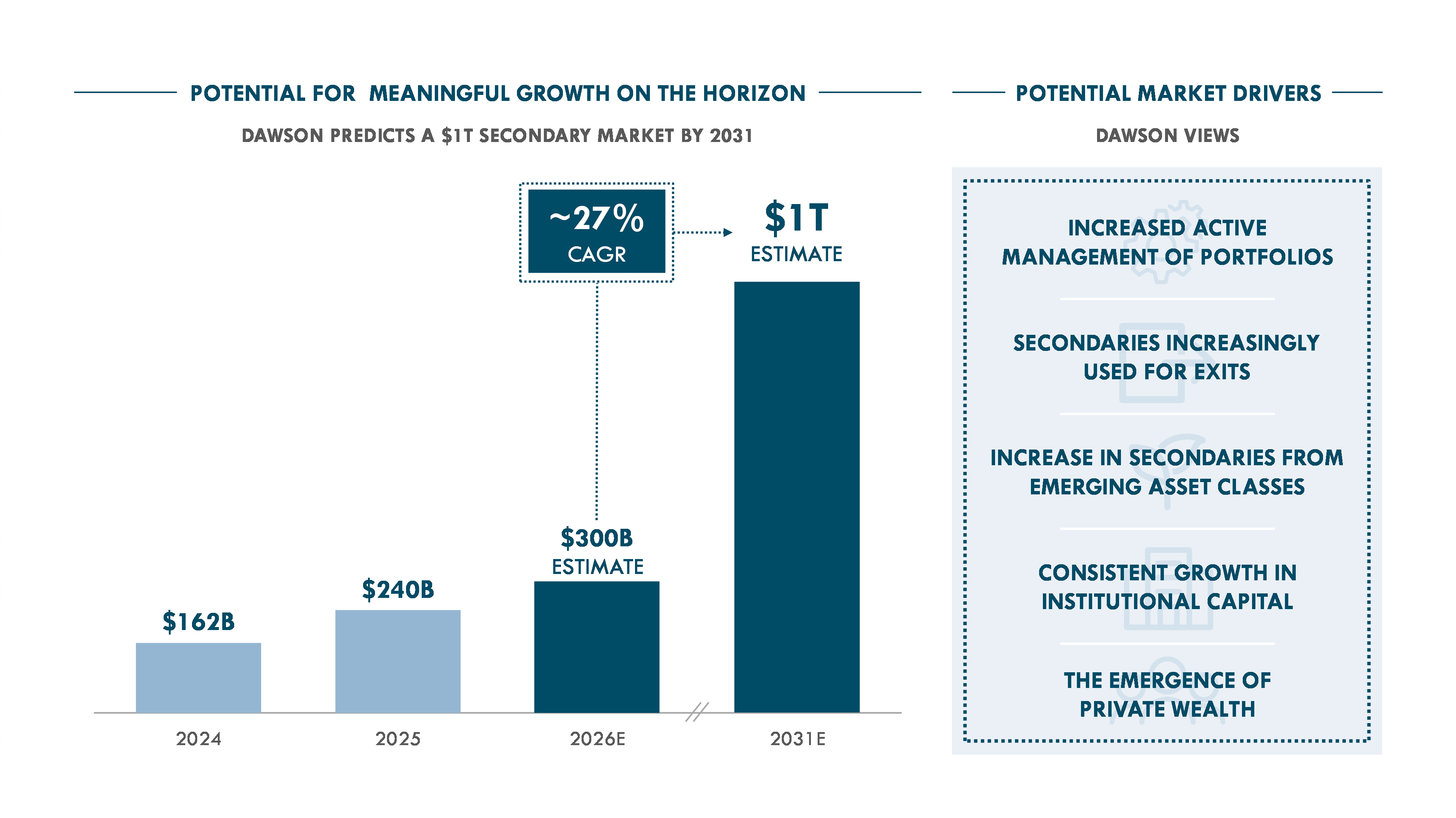

However, by the end of the Global Financial Crisis (“GFC”), the private markets secondary market had begun to institutionalize. As private market institutional portfolios grew in size and complexity, LPs increasingly sought out tools to actively manage exposures, rebalance portfolios, and respond to changing market conditions. This led to a further institutionalization of the secondary market, with transaction volumes reaching $23B in 2010 and continuing to grow steadily thereafter as the market matured. By 2025, global secondary market volumes had reached an all-time high of $240B with no signs of slowing, indicative of the increased acceptance of secondary solutions among market participants. A far cry from what the market looked like just two decades earlier.

As the market grew, so did the capitalization of the industry as it matured. Secondaries increasingly became an allocation within institutional portfolios. In 2024, roughly 60% of institutional LPs reported either a current or planned allocation to secondaries.1 What was once considered a niche solution has, for many investors, become a core portfolio management tool, and in tandem, many allocators have made significant commitments into the secondary market.

Source: (2001-2012): “A Primer for Today’s Secondary Private Equity Market” – CAIA (Q2 2018); Source (2013-2019): “2025 Secondary Market Highlights” – Evercore Private Capital Advisory (January 2026); Source (2020 – 2025): “Global Secondary Market Review” – Jefferies (January 2026). Refer to Legal Disclaimers below for more details.

Market Conditions Facing LPs

Large allocators like pension plans, endowments, insurers, sovereign wealth funds, and wealth platforms are navigating a challenging liquidity environment. Current conditions across private markets have exposed structural liquidity challenges.

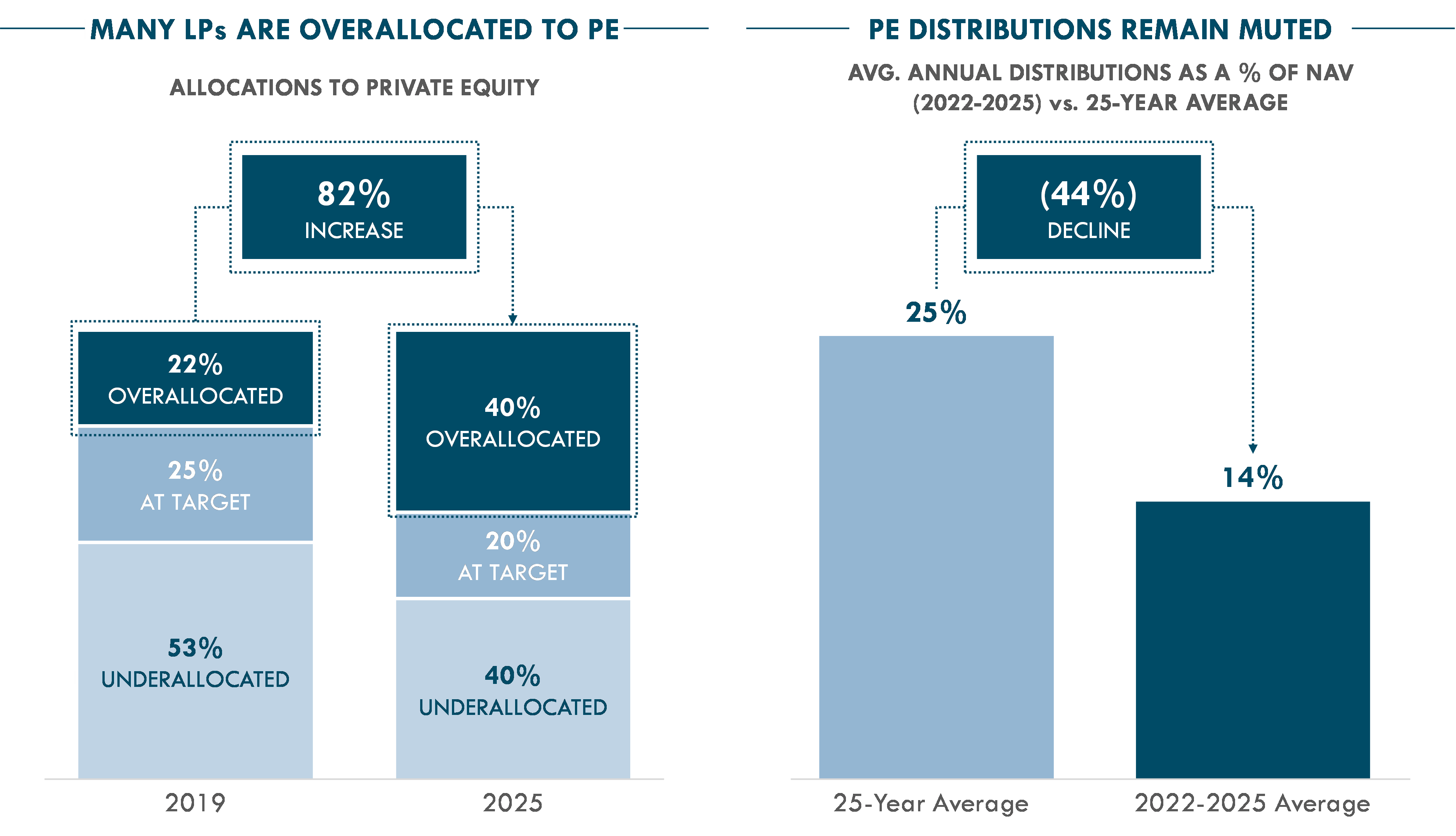

Distributions in private equity have sharply declined. On average, from 2001-2025, an LP could expect 25% of the net asset value (“NAV”) of their investment in a mature private equity portfolio to be distributed in a given year. From 2022-2025, that average was only 14% – a 44% decline. To put this into perspective, the four lowest distribution years over the last 15 years were 2022, 2023, 2024, and 2025 and there have only been three periods in the 21st century where the annual percentage of NAV returned to LPs was below 20% – the 2001-2002 dot-com bubble, the GFC in 2009 and now (2022-2025).2

These lower distributions have contributed to overallocation to private equity in LP portfolios. In 2025, 40% of institutional North American LPs reported being overallocated to private equity compared to 22% in 2019 – an 82% increase. LPs continue to face a lack of liquidity. One that, for many LPs, cannot be solved by simply waiting for an uptick in distributions from their portfolios. And furthermore, even if and when these distributions do ultimately pick back up… we may also see a corresponding increase in capital calls as broader dealmaking accelerates, in turn applying additional liquidity pressure on LPs.

To us, this all implies a state of overallocation in private equity for many LPs for the foreseeable future and points in the logical direction of LPs looking to the secondary market (or alternatives) for liquidity to help address that overallocation.

Source (2019 Overallocation): “Global Private Equity Report 2020” – Bain & Company; Source (2025 Overallocation): “A quarter of institutional LPs cut PE allocations in 2025” – Private Equity International (January 2026). Source (Distributions): MSCI Data. Refer to Legal Disclaimers below for more details.

Liquidity Options for LPs

Traditional Liquidity Options for LPs

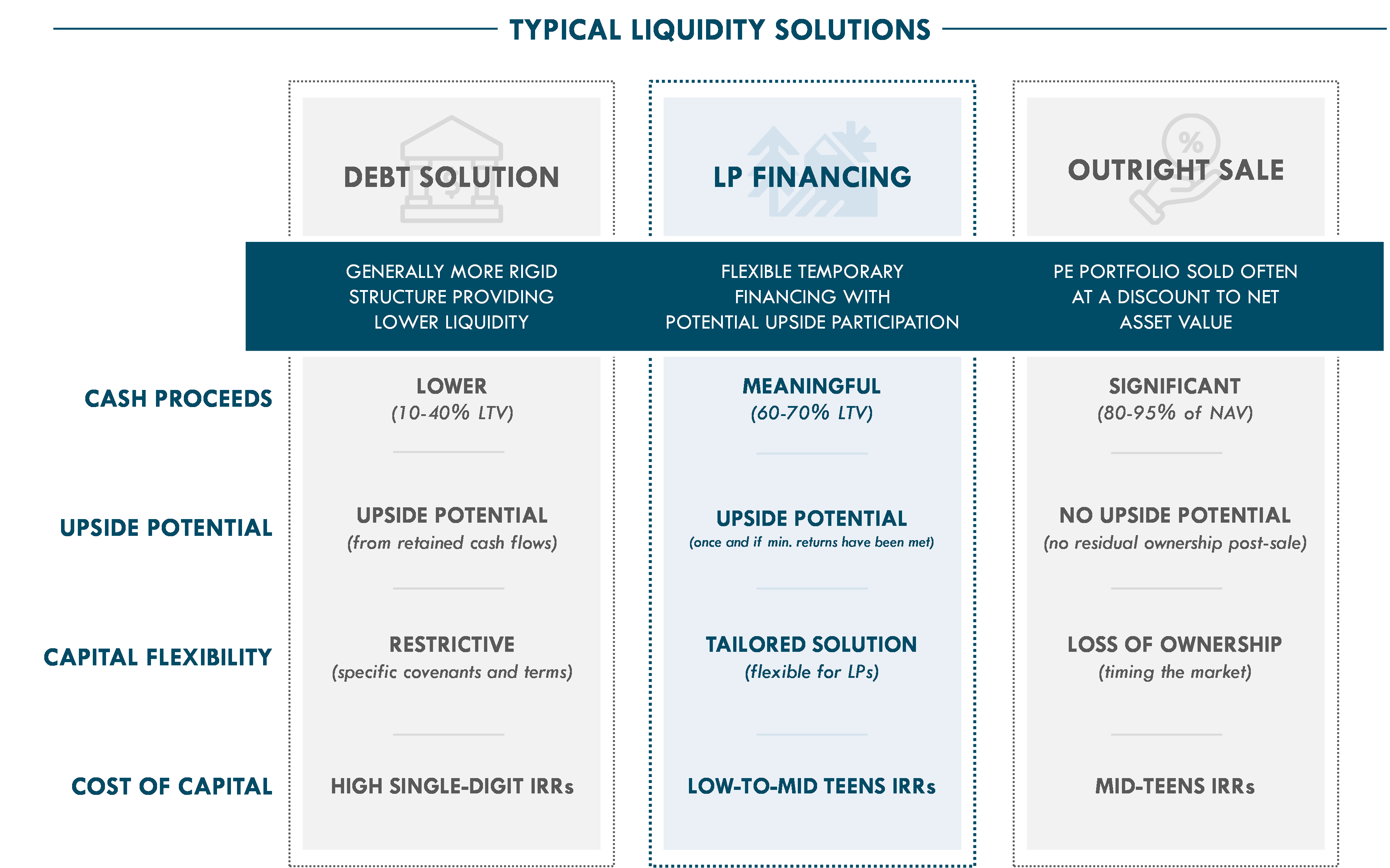

Traditionally, LPs seeking liquidity typically employ a familiar set of tools:

- Debt / NAV Lending: Banks and specialty lenders provide NAV-based loans secured against LP portfolios, generally advancing in the range of 10-40% loan-to-value (“LTV”). These facilities can be effective for short-term liquidity needs but may come with restrictive covenants, refinancing risk, and sensitivity to market/interest rate volatility and lower advance rates.

- Secondary Sale: LPs can alternatively sell their fund interests outright in the secondary market to create immediate liquidity. LPs frequently receive ~80-95% of NAV for buyout fund interests, which provides meaningful upfront liquidity but involves crystallizing a permanent discount on NAV and relinquishing any potential future upside in the fund’s performance.

The Limitations of Typical Liquidity Options for LPs

Both of these tools play an important role in the liquidity tool set for LPs looking to manage their portfolios but can fall short for one fundamental reason: lack of flexibility.

Traditional debt/NAV lending might not offer enough liquidity to address an LP’s needs and may come with restrictive covenants, maturity dates, upfront fees, and more. This can limit flexibility for LPs facing market volatility and balancing other strategic considerations.

In an outright sale of a fund interest, LPs typically sell at a discount to NAV, which would crystallize permanent losses. In addition, LPs forfeit any potential future upside and may risk impacting strategic relationships with their GPs – an increasingly important consideration as LPs seek co-investment opportunities.

In effect, both approaches may require that LPs time the market – by locking in a price or interest rate/spread at a certain point in time – rather than manage liquidity dynamically across cycles.

Emerging Need for Structured Solutions

Many LPs are searching for meaningful liquidity and the secondary market has been growing to address this, with no signs of slowing. As the secondary market has grown and as market participants have become more sophisticated, a broader spectrum of menu options to address these liquidity needs has emerged.

What we at Dawson call “LP Financing Solutions” have emerged as a natural evolution to add to this menu of alternatives. A structured solution that tends to sit in between the traditional debt and equity sale options, with the potential to mitigate some of the drawbacks of both of those options.

In many respects, LP Financing Solutions represent an evolution of liquidity management in private markets as they offer a flexible, innovative pathway to liquidity that does not require LPs to choose either incurring leverage or exiting their positions altogether.

What Are LP Financing Solutions and Why Do They Matter?

Key Features of LP Financing Solutions

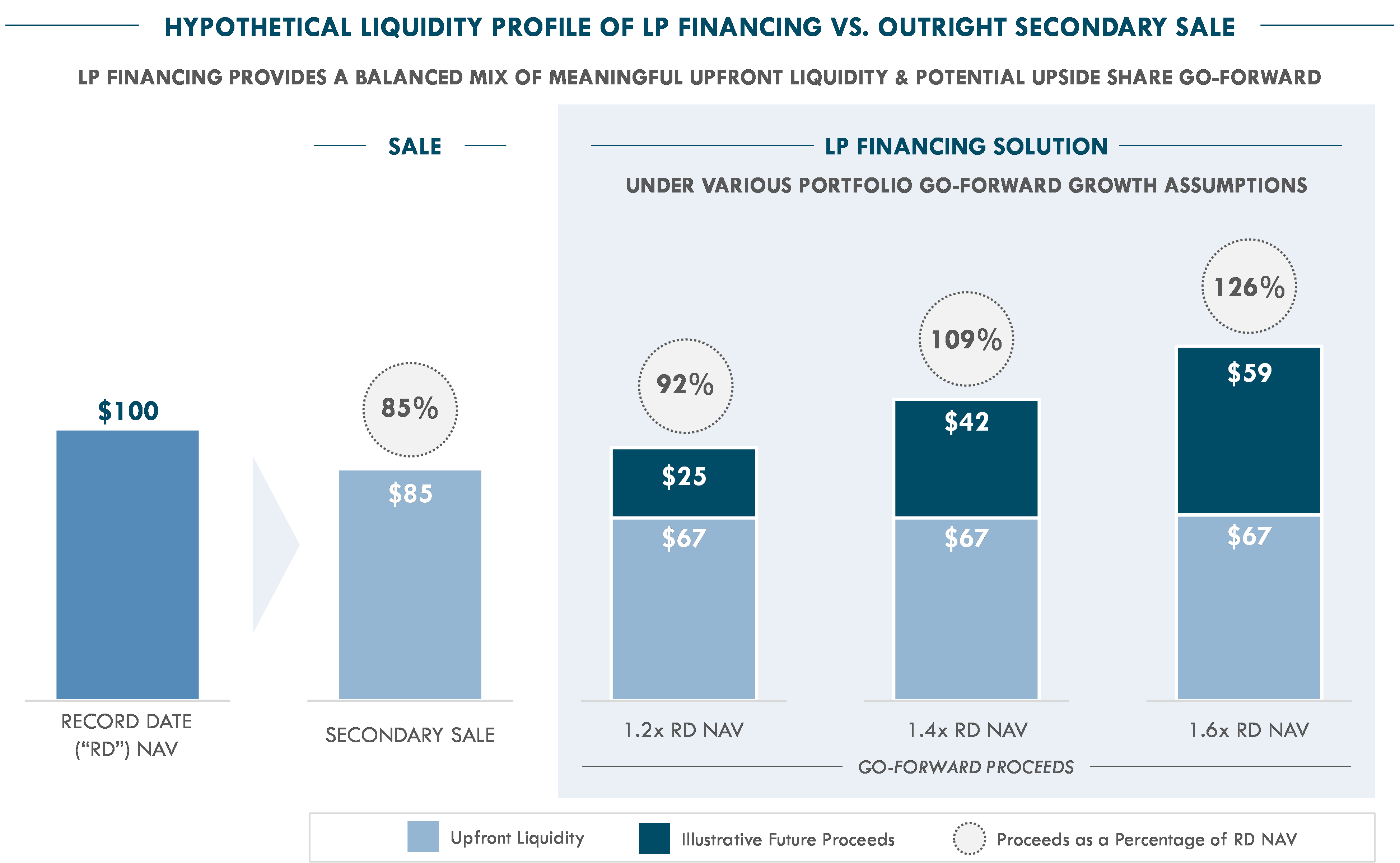

In a typical LP Financing Solution construct, a provider will advance liquidity to an LP against a portfolio of their existing LP interests, typically private equity fund interests. In exchange for that advance, the solution provider will sweep cash flows from the collateral portfolio until certain minimum returns are achieved.

Once and if these minimum returns are achieved, the LP and the provider will split go-forward cash flows, typically with the majority of that upside going to the LP. This structure provides the potential for an LP to satisfy their near-term liquidity needs while maintaining exposure to a portion of any future upside in the portfolio, which would otherwise be forfeited in an outright sale of those fund interests. In fact, should the portfolio perform above a certain level go-forward, an LP might end up with returns in excess of NAV because of their share in any future upside.

Calculations are based on: (i) an illustrative portfolio with $100M of record-date NAV; (ii) an illustrative secondary sale priced at 85% of record date NAV; and (iii) an illustrative LP Financing Solution with upfront liquidity equal to 67% of record date NAV, 100% of distributions to the solution provider until a 1.35x multiple and then a cash flow split – 15% to the solution provider and 85% to the LP. The LP Financing Solution is shown across three illustrative scenarios with different portfolio go-forward growth assumptions. Refer to the Legal Disclaimers below for additional details.

How LPs Use LP Financing Solutions

These solutions provide flexible capital that can be used to satisfy a range of strategic objectives, including:

- Managing Overallocations: LPs can reduce private equity exposure by reallocating upfront liquidity to other asset classes without reducing long-term exposure to key relationships or managers that they retain high conviction in.

- Cash Needs: Provides meaningful upfront liquidity that can help LPs address immediate liquidity needs without having to time the market as to the best time to sell.

- Portfolio Rebalancing: LPs can use these solutions to rebalance their portfolios across vintage, manager, geography, or sectors without triggering permanent losses.

- Tactical Reallocation: LPs can use liquidity to redeploy into higher-conviction opportunities like co-investments, new GP relationships, or thematic strategies without losing their relationship with an underlying GP, which might occur in an outright sale.

LP Financing Solutions are a nuanced tool that enable more deliberate, portfolio-level decision making.

Refer to Legal Disclaimers below for more details.

Implications for LPs and GPs: A Potential Win-Win Scenario

For LPs Seeking Liquidity

LPs using LP Financing Solutions are able to solve liquidity or portfolio rebalancing needs while maintaining strategic relationships with key GPs, retaining a share of potential upside in their portfolios, and avoiding crystallizing permanent losses at a particular time in the market (assuming sale at a discount to NAV).

For GPs

From the perspective of GPs of funds in the portfolio of an LP engaging in an LP Financing Solution, they are able to retain more stability within their investor base – typically preferred to an LP outright selling their commitment. LPs that use these LP Financing Solutions often also remain committed to a GP’s long-term strategy rather than exiting their fund – minimizing the potential disruption to the fund-level ownership of that GP’s current or future to-be-raised funds.

For Those Who Invest in These Types of Solutions

LP Financing Solutions present an interesting opportunity for investors and have the potential to offer a hybrid return profile, often thought of as a private credit-like investment. LP Financing Solutions have the potential to provide (i) contractual enhanced downside protection and embedded asset coverage due to the potentially meaningful LTV advance rate, (ii) a priority cash flow arrangement which can offer an accelerated path to liquidity, and (iii) increased alignment between LPs and LP Financing Solutions providers given the split share of potential upside once and if minimum returns are met.

Structured with the objective of withstanding volatility, LP Financing Solutions have the potential to provide a complementary return profile to more traditional investments – seeking to offer the downside protection of other credit-like investments while offering the opportunity to share in any potential upside of a portfolio.

New Use Cases Emerging

Beyond providing upfront liquidity to LPs, LP Financing Solutions can support broader active portfolio management.

Using these solutions, LPs may be able to tactically shift exposure from one asset (or sub-asset) class to another to align with thematic market views. Additionally, some LPs may use these solutions to generate liquidity in order to invest in other opportunities, including to bolster the target return profile of their private equity programs. And with increasing sophistication in deal construction, LP Financing Solutions as a strategy may evolve further with the inclusion of unfunded capital in the collateral pool, which can be additive to LPs by enabling future deployment.

While LP Financing Solutions help LPs solve for today’s challenges, they can also increase future flexibility and support strategic decisions.

A Continued Demand for LP Financing Solutions

Market trends suggest that demand for secondary solutions, including LP Financing Solutions, will persist. Many LPs remain overallocated to private equity and need tools to rebalance over the long term, not just for the next few quarters. Distribution levels remain below historical averages and a return to average liquidity may take time. Yet many GPs are returning to market faster and with larger fund sizes – potentially creating liquidity mismatches for certain LPs and driving the opportunity for these solutions today.

In fact, at Dawson we deployed $3.2B into these solutions over the last 18-months alone. But readers would be wrong to think these opportunities only exist in low-liquidity markets. Over the long-term, additional key drivers of growth are emerging – including increasing use of active portfolio management by LPs and the participation of new sellers from growing areas of the allocator market. These solutions are starting to become a true all-weather tool in the liquidity tool set for LPs.

Source (2024-2025): “Global Secondary Market Review” – Jefferies (January 2026). Refer to Legal Disclaimers below for more details.

Conclusion

LP Financing Solutions have become an effective tool for navigating today’s liquidity-constrained environment and addressing LPs’ increasing desire for active portfolio management.

By offering meaningful upfront liquidity without forcing permanent exits or imposing restrictive leverage covenants, these solutions allow LPs to achieve liquidity needs while maintaining manager relationships, preserving more upside potential, and without crystallizing a discount via an outright sale.

For LPs seeking to manage portfolios dynamically across cycles, LP Financing Solutions represent not just an alternative, but an increasingly important tool.

1Source: “LP Perspectives 2024” – Private Equity International

2 Source: MSCI data as of January 31, 2026 for 2001-2024 (i.e., most recently available data). 2025 figure represents the passive unstructured distributions over NAV of closed transactions in Dawson’s vehicles, given MSCI data for 2025 is not yet available. Selection criteria based on Dawson views.

Legal Disclaimer: Based upon Dawson’s current views informed by published sources and third parties outside Dawson. No assurances can be made that historical trends will continue or that expectations will materialize. Past performance is not indicative of future results. Chart 2.0: Source (Avg. Annual % of NAV Returned): MSCI data as of January 31, 2026 for 2001-2025Q3 Annualized (i.e., most recently available data). Reflects data for 50th percentile North American buyout funds greater than $250M and represents annual average of fund vintages that are 3 to 10 years old. Different criteria would have yielded different results. Dawson would be pleased to discuss criteria further. 15-year average represents average annual percentage of NAV returned from 2011 – 2025. Chart 3.0 is provided for illustrative and informational purposes only, and not intended as an offer to transact or invest. Dawson illustrative scenarios remain subject to further diligence. They are subject to uncertainties, changes and other risk. There can be no assurance that comparable outcomes will be achieved, that assumptions will come to fruition or that any liquidity solution will be accretive. Chart 4.0 is provided for illustrative purposes only. The opinions expressed are solely Dawson’s opinions, informed by published sources and third parties outside Dawson, and should not be relied upon in connection with any investment decision. There can be no assurance that any such opinions will prove correct. The comparison chart is included to show certain characteristics selected by Dawson of three different liquidity solutions. The characteristics were selected based on criteria that Dawson believes to be important. Reasonable parties may disagree with the selections or characterizations. Different selections or characterizations may yield different results. Chart 5.0: 2026 and 2031 estimates are based upon Dawson’s current views informed by published sources and third parties outside Dawson, and no assurances can be made that these expectations will materialize. As a result, undue reliance should not be placed on expectations.