Hedge funds have had a quite a streak in delivering on their promises to investors in recent years, but they’re not invincible.

Few strategies have emerged unscathed after the Iran war and the skyrocketing price of oil sent markets reeling last month. Both the Nasdaq and the Dow Industrials fell into correction territory and all sectors of the S&P 500 fell, except energy. Treasurys also dropped right along with stocks. Traders with bets that interest rates would fall were stymied by the prospect of higher inflation from snarled supply chains and soaring gas prices.

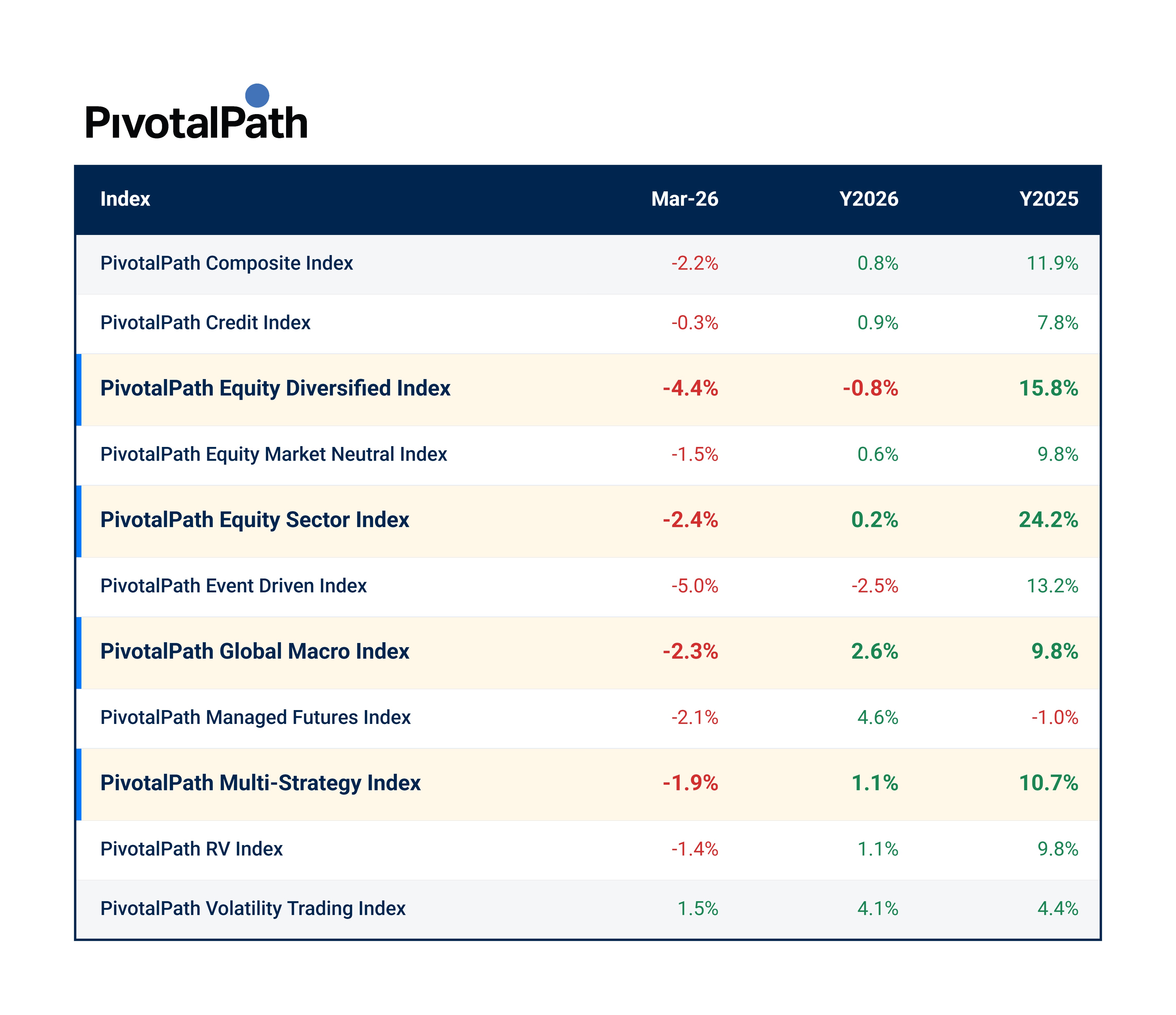

Long-only hedge funds that invest in a diversified mix of stocks posted their worst month since the early days of the pandemic, while macro and multi-strategy funds proved more resilient, according to an early look provided to II on PivotalPath's March indices. The Equity Diversified Index was down 4.4 percent, compared to 8.39 percent in March 2020. The Equity Sector Index held up better (down 2.4 percent), helped by some energy and healthcare funds that were able to navigate the dispersion in stocks. Equity Diversified was up 15.8 percent in 2025, while Equity Sector funds were up 24.2 percent.

(Click here for the latest index performance data and access to PivotalPath's full suite of hedge fund indices.)

PivotalPath's Global Macro Index was down 2.3 percent, but still up 2.6 percent year-to-date. Global Macro funds were one of the best performing categories in 2025, up 9.8 percent. Funds with significant long exposure to equities were hurt, while a number were also hit by their bets on rate cuts in the U.S. and Europe, according to Caplis.

One of the most consistently strong-performing categories — multi-strategy — was down 1.9 percent last month. A number of funds managed to insulate themselves from losses, especially those with more systematic strategies, according to PivotalPath. But multi-strat platforms that were on the wrong side of the oil/inflation shock and which also had heavy exposure to the equity and bond sell-off suffered. Multi-strats generated 10.7 percent in 2025.

The Relative Value index, which represents hedge funds that are designed to truly hedge portfolios, was down 1.4 percent for the month. In 2025, the RV index returned 9.8 percent.

Markets have long been — perhaps, always — tethered to energy prices. Institutional Investor reported early last month on PivotalPath’s historical research showing the connection in vivid detail. Managed futures and global macro commodities funds are two strategies that tend to do well when oil prices spike. When crude traded between $100 and $140 per barrel, managed futures funds rose 9.1 percent on an annualized basis and global macro commodities strategies gained 8.8 percent annualized, while the S&P 500 fell 1.6 percent. Of course, as the March data shows, the effect is not “instantaneous,” Caplis pointed out. In March, managed futures funds lost 2.1 percent and global macro funds were down 2.3 percent.

Unfortunately, what happened in March and in April so far — a tragic war, an energy crisis — won’t be the last. The best investors can do is understand how their funds should behave at different points in the market and if they stray, why.